Disclaimer: This article is intended to only to assist you in understanding possibilities. I am neither a lawyer nor investment adviser. None of this information is intended to serve as legal, tax or financial advice. I do not put any guarantees on this information and am not liable for any action you take or fail to take based on information that exists on this site.

Consult with an attorney, CPA, and/or investment adviser before pursuing any action.

Audience

Stockholders of companies that have recently IPO'd subject to lock-up that wish to hedge their risk.

The audience excludes current employees of the recently IPOd company as the Insider Trading Policy almost certainly precludes them from any form of hedging.

Lockups 101

Typically at IPO, every pre-IPO stock holder is banned from selling for 180 days. Without going into too much detail, this is because the IPO underwriter wants an IPO that goes up in price, not down. Read about Greenshoeing if you want to know more.

Because of this practice, venture backed company equity agreements given to all stock holders (e.g. employees) include “market standoff” agreements that prohibit selling (such language being in stockholder agreements is presumably necessary for underwriters to agree to an IPO). Additionally, the company can take reasonable actions to make selling difficult, such as requiring your stock be held in a custodian of their choosing, wherein selling is disallowed.

(Additionally, larger holders, typically investors that participated in formal financing holds, sign a separate lockup agreement that may have tighter restrictions than the “market standoff” agreement in the original equity agreement.)

Why hedge?

- Because you would have sold stock immediately if you allowed to. See the sell timing overview.

- VC-funded stocks fall an average of 3% at lock-up expiry. Hedging can help you get ahead of this.

Can you hedge?

You might be able to hedge your stock. Read the market standoff agreement section of your equity agreement for what is prohibited.

The restrictions that may exist, ordered from least to most restrictive

- No bans. Perhaps you don’t even have a lock-up in which case none of this applies. This is highly unlikely.

- Ban only on selling. This was mine. If you take a reasonably conservative definition of what

“selling” means, this means you can hedge, but

you shouldn’t do any form of constructive

sale (explained extensively in this post).

- Example language: “Participant will not sell or otherwise dispose of shares of the Company’s Common Stock without the prior written consent of the Company or such underwriters”

- Ban selling + writing call options.

- Expressed by blocking the “granting any option for the purchase of” stock or “selling any option or contract to purchase” stock.

- Ban selling + all options: A restriction this tight bans all hedging.

- Wealthfront has example language: “purchase any option or contract to sell”

Checking further

Violating your market standoff agreement’s restrictions could lead to you being sued. I recommend contacting your company’s equity operations team to verify if your interpretation of your contract is correct. If you disagree with your company, you may wish to consult a securities lawyer.

Are you an employee?

Check your Insider Trading Agreement. It probably bans derivative trading. Not because the SEC cares, but because the company doesn’t want you to be able to “bet against the company” and have misaligned incentives.

The best you can do as an employee (aside from quitting to relieve yourself of the Insider Trading Agreement’s restriction) to hedge your risk is to buy protecting options on the overall sector your company is in (while you can’t reduce company specific risks, you can reduce sector or macro-economic specific risks).

Put options 101

The standard way to hedge is to use options, which were designed specifically for hedging risks on the underlying stock. This section will dive into purchasing insurance on the downside risks (“put options”), which is more likely to be permitted. The next post discusses writing call options, a more advanced strategy, that is less likely to be permitted by your market standoff agreement.

A put option gives you the right, but not obligation, to sell a stock at a given price, before some expiration date. When you hold the underlying shares, this is known as having a “protective put”.

- You must pay to purchase a put. (the price is known as a “premium”)

- If at expiration, the stock trades below the strike, you can “exercise” the put, selling the stock at the put strike price.

- If at expiration, the stock trades above the strike, the put expires unused and you only lose the premium you paid.

- The put was “worth doing” if at expiration, the stock trades below the strike less premium (the “minimum take-away”)

Here’s an example of the pay-off when stock is protected by a put option. Note that upside is decreased by the price of the put, but that the put provides a floor on the stock’s value.

Cost

The price of a put is determined by the Black-Scholes formula. Generally speaking, a put option with a strike equal to the current price and expires in six months, will cost about 15% of the underlying value. (e.g. put with a strike of $100 on $100 stock would cost about $15).

You can calculate the price of a put here. Use 0.024 (2.4%) as risk-free rate (current 30 day daily treasury yield) and 0.6 (60%) as a reasonable number for annual volatility if an options market doesn’t yet exist for your stock.

The lower the strike price of your put, the cheaper it will be.

Theory

This section assumes undergraduate-level probability knowledge

The log of a stock return over any time period is may be modeled as a normal distribution (this is known as “lognormal”). (yes, this is a very simplified model of the real world.) Different stocks have different volatility (standard deviation of annual returns), leading to wider ranges of returns.

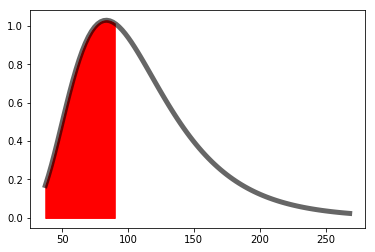

Here’s the probability distribution function (pdf) of a stock’s share price in 6 months currently trading at $100/share with an annualized volatility of 60% [1]:

Purchasing a put option is analogous to buying an insurance plan. If you buy a put option with a strike at $90, the option ensures you can’t end up with less than $90 (which has an odds of about 40%). That is in the figure below, any outcome in the red has a value of $90.

If the put cost $11 (which Black-Scholes predicts), this was a profitable hedge if the stock dives under $79 (29% chance).

You have increased the expectation of your returns by $11 - exactly equal to the put premium you paid. (And because your risk is now lower, your risk-adjusted returns are higher). [2]

Executing

Got a lot of stock?

If you have a huge amount of stock, say over $5M, you can stop here. Your best bet at this point is to contact an investment bank and ask to hedge. A custom solution may be cheaper and easier to execute than using a broker to hedge millions of equity.

Put options look too complicated/too expensive?

Consider using Stock Protection Funds instead.

Otherwise..

Have a brokerage account

First, you are going to need a brokerage account and get approved for options. You need to be approved for whatever level allows you to buy uncovered put options. (the broker doesn't know you own the stock elsewhere!).

Funding

As mentioned above, covering your entire position can be expensive. To obtain the cash:

- Sell assets with little capital gains and use proceeds to buy puts

- Get a 0% APR for 15+ months credit card with a very high credit line. Direct all purchases to that card.

- Take a margin loan against your brokerage assets. Iteractive Brokers offers very low margin rates (<4% APR) You need to be careful to understand your risk of being margin called.

- Take out a HELOC against your home (typically ~5% interest rates).

- Take out a personal loan (typically ~7% interest rates). Sofi and Lightstream have

the highest caps ($100k) and generally lowest interest rates if you have excellent credit.

- High credit card debt will hurt your credit score, so don’t start using your high credit line on the 0% APR card until you are approved for the loan.

- Once you take out $100k in loans, your credit score will take a hit. (until it is paid back). From my experience, borrowing over $200k is not practical due to interest rate jumps/approval difficulties following the credit score hit.

Trading

- Figure out how to buy options with your broker.

- Find the options that expire the soonest after your lock-up ends.

- Ones that expire before won’t hedge you through the lock-up!

- Ones further out are more expensive as you get unnecessary protection (into a time when you should just sell).

- Remember that 1 put contract protects 100 shares.

- The pricing for options is given per share, but you must buy the options in units of 100 shares!

- Only buy out-of-money put options (strike price below current) to ensure you are not constructively selling.

- Some tax practitioners believe that buying in the money (or very deeply in the money) put options are a form of constructively selling. Consequently, buying such puts might violate your contract to not “sell”.

- Purchase with limit orders or “walk limit orders”. The market is illiquid and you are likely purchasing from market makers - you’ll want to test what pricing they are willing to sell the put options to you for.

At end of lockup

At end of lockup, ACAT your stock into your brokerage account. Simultaneously dispose stock with the offsetting, hedging options:

- If all went well, your stock is above the put strike price — just sell the puts back (they’ll likely still have some “time value”) as well.

- If things went badly and the stock is below the put strike price, determine the time value of the option and

do one of the following:

- Time value exceeds trading cost: Sell the put

- Time value less than trading cost: Exercise the put

- Note that exercising the put can have favorable tax rates compared to selling; see tax implications below.

Tax implications

Have familiarity with investment taxes.

Options

Protected puts on stock create what is known as a straddle. These are IRS rules that are in place to prevent people from employing creative means with options to either defer losses or reduce risk of getting long-term cap gains. Generally, I recommend consulting an accountant here if you aren’t comfortable following Pub 550's rules.

In a nut shell:

- If the stock you are straddling is not yet eligible for long-term capital gains, you reset the holding

clock.

- If you have any short-term stock you wish to wait on selling until long-term capital gains, you need to identify your straddles as not affecting that stock. A reasonable straddle identification is a 1:1 map. (X put contracts (worth 100 shares) straddle these specific 100 shares).

- Gains on the options are short-term gains (rather than more valuable long-term gains).

- exception: If you exercise the put with long-term held stock, the “gain” on the put is effectively long-term.

- If you straddle long-term held stock, losses on the options are long-term losses (rather than more valuable short-term losses).

- The IRS will not allow you to sell one leg (e.g. options) for a loss in one year and the other leg (e.g. stock) for a gain the next; any loss is deferred until all legs are disposed.

- Capital gains from straddled stock/option cannot be invested into opportunity zone funds.

- At tax time, you may need to report the straddles on Form 6781, Part II.

Interest deduction

You can deduct the interest on any loan used to purchase the put options (“investment interest”). This interest will be “capitalized” into your straddles (basically this means your interest is deducted at short-term rates for short-term straddles and long-term rates for long-term straddles).

Can you write calls?

If your contract allows you to write calls, you can hedge cheaper, perhaps at no-cost. Read More

Notes

[1] Probabilities in this article don’t account for excess returns over the risk-free rate due to owning a risky asset (CAPM prediction)

[2] Because the risky asset you own has positive expected returns (relative to risk-free rate), but the put option is priced as though it doesn’t, you actually in a sense “overpay” for the put (the stock is less likely to be at $90 at the terminus than the put option pricing implies). Consequently, with a put your expected return is lowering, a fact further enhanced by the trading costs (bid/ask spread and commissions) of acquiring the puts. However, in a case where you hold far too much of this risky asset, it will be true that buying the put is cutting your volatility more than expected return, meaning you’ve increased your risk-adjusted expected returns.