Disclaimer: This article is intended to only to assist you in understanding possibilities. I am neither a lawyer nor investment adviser. None of this information is intended to serve as legal, tax or financial advice. I do not put any guarantees on this information and am not liable for any action you take or fail to take based on information that exists on this site.

Consult with an attorney, CPA, and/or investment adviser before pursuing any action.

Overview

As discussed in the prior post, buying a put can be expensive. e.g. a put with a strike 10% below current price might cost 10% of your current asset value.

If your market standoff agreement permits you to write options (remember to validate with your company's equity operations and/or a lawyer), you can pay for the put option with your “upside” rather than money.

Call options 101

A call option gives the holder the right, but not obligation, to buy a stock at a given price, before some

expiration date.

For the purposes of hedging, you’ll be writing (selling) the call. When you hold the underlying shares, this is

known as having a “covered call”.

- You receive a premium when you sell the call.

- If at expiration, if the stock trades above the strike, the holder will exercise it (buying your stock at the strike price)

- If at expiration, the stock trades below the strike, the call expires unused and you gained the premium.

- Writing the call was “worth doing” if at expiration, the stock trades below the strike plus premium received.

Fun fact: Employee stock options are call options with a very far out expiration date.

The collar

By using the proceeds of the call option to purchase a put option, you can hedge for no cost!

In effect, you’ve sold your upside to protect your downside. Your stock probability distribution (described earlier) now looks like this:

- If the stock ends up in the red (below $90), you can sell for $90 (insurance!)

- If the stock ends up int the blue (above $111), you earn no profit above $111 (upside lost)

- Overall, risk is drastically cut.

Executing

First Understand the basic steps.

On constructive sales

As discussed earlier, to be conservative with your agreement, don’t constructively sell. You have constructively sold your asset if you effectively have ceased taking risk on the stock your options "straddle". Example:

- Stock at $100

- Write a call for $100

- Buy a put at $100

No matter what, you walk away with $100. You’ve “sold” (constructively).

Many accounting practitioners believe the collar band (call strike less put strike) must be at least 15% of the underlying value to not be a constructive sale. This means that in practice, you’ll need to accept a 7% downside risk or so on a zero-cost collar.

Got a lot of stock?

Again, if you have over $5M of stock, stop here and contact an investment bank. They may be willing to sell you a collar directly. If you have under $5M, they likely won’t be interested enough to bother.

Margin Trading

In the ideal world, you will have the shares in the same account you are writing the calls. If this is true, there is no margin hit — the broker understands that the calls are backed by your stock.

However, during lockup, you are very unlikely to be able to trade in the account that holds your stock. From the brokers point of view, your calls are not backed by stock — they are naked calls. Consequently, you'll be using margin.

Do not write naked calls! If the stock goes up, the broker owning your options will think you are losing — and you might getmargin called. This might force you to sell your calls at a loss and if the stock dives back down - you end up in a much worse place than when you started: “whipsawed”.

Bear call Spread

To avoid writing naked calls (with unlimited downside), you are going to buy a call option (a “long call”) that is at a even higher strike price. You thus will have a protective put plus a bear call spread.

For instance, if you wrote a call at a $111 strike and buy a call at a $141 strike:

- Your maximum loss (from the broker’s POV) is $30. If the stock finishes above $121, you can always exercise your call.

- Your net premium received is positive: The $111 call is worth more than the $141 call.

- For 6 month expiry when stock is currently $100, Black-Scholes predicts $13 premium on $111 call and $6 premium on $141 call, leaving a net premium of $6.

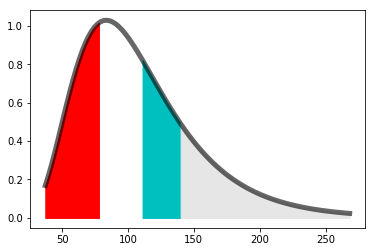

Example return:

- If the stock finishes in red, you can sell at $90 (border between white and red)

- If the stock finishes in the blue, you must sell at $111 (border between blue and white)

- If stock finishes in the grey, you must sell at $111, but can also can buy a new share at $141 (border

between blue and grey) and immediately resell it.

- i.e. your net sales price is current price less $30.

Structuring your hedge

You have a few parameters to play with:

Long call price You’ll generally want the maximum distance between the long call and the written call (since you aren’t concerned with capturing the extreme upside). This is limited by your capital; borrowing money becomes much more important than with puts alone. Determine the available margin basis points you can safely consume (less the ones going to puts!) and divide by the number of shares you wish to protect. That will give you the distance between the two strikes.

Zero-cost or pay? Because you need to pay for the long call, you’ll have less premium to buy the put option. You can either:

- Spend money to have a higher put strike. (the bear call spread does help offset the price!)

- Lower your put strike. For instance with a $6 premium received, you can buy a $78 put (rather than a $94 strike put you could have bought for $13).

When trading, many brokers offer the ability to buy multiple options as a single "all or nothing" transaction

Assignment Risk

If the stock goes up and your out-of-money call options goes into the money, it is possible that the holder will early-exercise it (This is called being assigned), which will leave you with a short position on the stock. In practice with a non-dividend paying stock, this is pretty unlikely to happen unless the call goes so deep into the money and is so close to expiry that the difference between the asset price (spot) and strike price is close to the premium.

- If the price does go up, consider closing your original collar and buying one at the higher value to mitigate this risk.

- If you are assigned, just buy back the short position — and then close/re-open the collar as mentioned above.

Tax implications

This is just a more complex straddle than the protected puts described earlier.

Interest deduction

Excess investment interest needed to “hold” your asset positions (had you liquidated them, you’d have more margin BP) can be deducted on schedule A.